再帰的最小二乗法¶

再帰的最小二乗法は、通常の最小二乗法の拡張ウィンドウ版です。再帰的に計算された回帰係数に加えて、再帰的に計算された残差は、パラメータの不安定性を調査するための統計量の構築に使用されます。

RecursiveLSクラスは、再帰的残差の計算を可能にし、CUSUMおよびCUSUMの二乗統計量を計算します。これらの統計量を、パラメータの安定性という帰無仮説からの統計的に有意な偏差を示す参照線と一緒にプロットすることで、パラメータの安定性を視覚的に簡単に確認することができます。

最後に、RecursiveLSモデルは、パラメータベクトルに対して線形制約を課すことができ、式インターフェースを使用して構築することができます。

[1]:

%matplotlib inline

import matplotlib.pyplot as plt

import numpy as np

import pandas as pd

import statsmodels.api as sm

from pandas_datareader.data import DataReader

np.set_printoptions(suppress=True)

例1: 銅¶

まず、銅データセットのパラメータの安定性を検討します (説明は下記)。

[2]:

print(sm.datasets.copper.DESCRLONG)

dta = sm.datasets.copper.load_pandas().data

dta.index = pd.date_range("1951-01-01", "1975-01-01", freq="AS")

endog = dta["WORLDCONSUMPTION"]

# To the regressors in the dataset, we add a column of ones for an intercept

exog = sm.add_constant(

dta[["COPPERPRICE", "INCOMEINDEX", "ALUMPRICE", "INVENTORYINDEX"]]

)

このデータは、1951年から1975年までの世界の銅市場を記述したものです。Gillの例

では、2段階推定の結果変数として、25年間の世界の銅消費量が使用されています。

説明変数には、以下が含まれます:

- 世界の銅消費量(単位: 1000メートルトン)

- 調整済みの実質ドルベースの銅価格

- 代替品であるアルミニウムの価格

- 1970年を基準とした1人当たり実質所得の指数

- 製造業の在庫変動の年間測定値

- 時間のトレンド

次の警告が表示されます:

C:\Users\user\AppData\Local\Temp\ipykernel_15324\2153377698.py:4: FutureWarning: 'AS' is deprecated and will be removed in a future version, please use 'YS' instead.

dta.index = pd.date_range("1951-01-01", "1975-01-01", freq="AS")

**警告の意味**: `AS`(年単位の開始日を指定する頻度)が廃止予定で、将来のバージョンで削除されるため、

代わりに`YS`(同等の機能を持つ頻度)を使用するよう推奨されています。

まず、モデルを構築してフィットさせ、要約を出力します。RLSモデルは回帰パラメータを再帰的に計算するため、データポイントの数と同じ数の推定値がありますが、要約テーブルにはサンプル全体で推定された回帰パラメータのみが表示されます。再帰の初期化による小さな影響を除けば、これらの推定値は OLS 推定値と同等です。

[3]:

mod = sm.RecursiveLS(endog, exog)

res = mod.fit()

print(res.summary())

Statespace Model Results

==============================================================================

Dep. Variable: WORLDCONSUMPTION No. Observations: 25

Model: RecursiveLS Log Likelihood -154.720

Date: Thu, 28 Nov 2024 R-squared: 0.965

Time: 23:11:12 AIC 319.441

Sample: 01-01-1951 BIC 325.535

- 01-01-1975 HQIC 321.131

Covariance Type: nonrobust Scale 117717.127

==================================================================================

coef std err z P>|z| [0.025 0.975]

----------------------------------------------------------------------------------

const -6562.3719 2378.939 -2.759 0.006 -1.12e+04 -1899.737

COPPERPRICE -13.8132 15.041 -0.918 0.358 -43.292 15.666

INCOMEINDEX 1.21e+04 763.401 15.853 0.000 1.06e+04 1.36e+04

ALUMPRICE 70.4146 32.678 2.155 0.031 6.367 134.462

INVENTORYINDEX 311.7330 2130.084 0.146 0.884 -3863.155 4486.621

===================================================================================

Ljung-Box (L1) (Q): 2.17 Jarque-Bera (JB): 1.70

Prob(Q): 0.14 Prob(JB): 0.43

Heteroskedasticity (H): 3.38 Skew: -0.67

Prob(H) (two-sided): 0.13 Kurtosis: 2.53

===================================================================================

Warnings:

[1] Parameters and covariance matrix estimates are RLS estimates conditional on the entire sample.

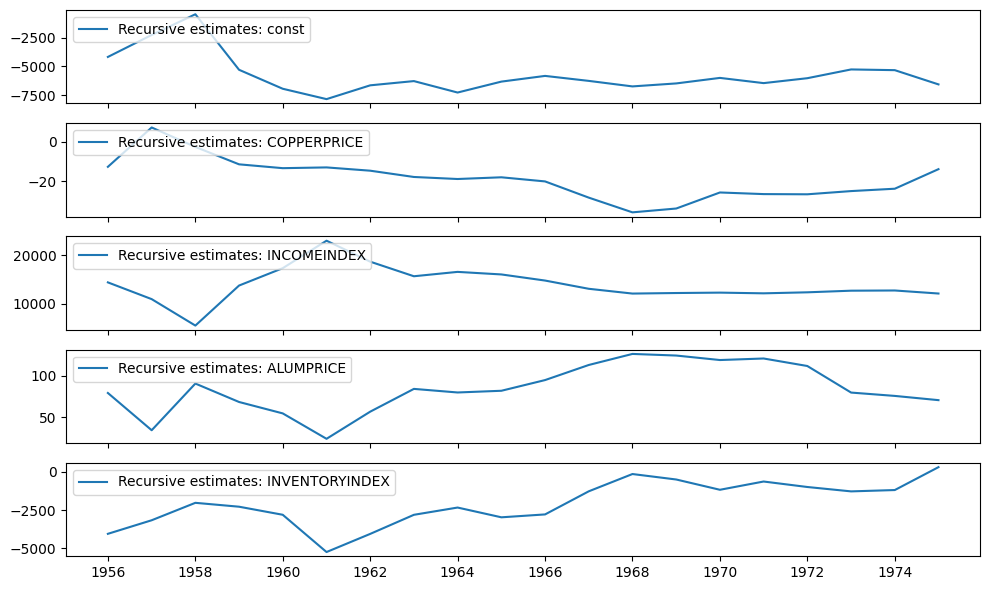

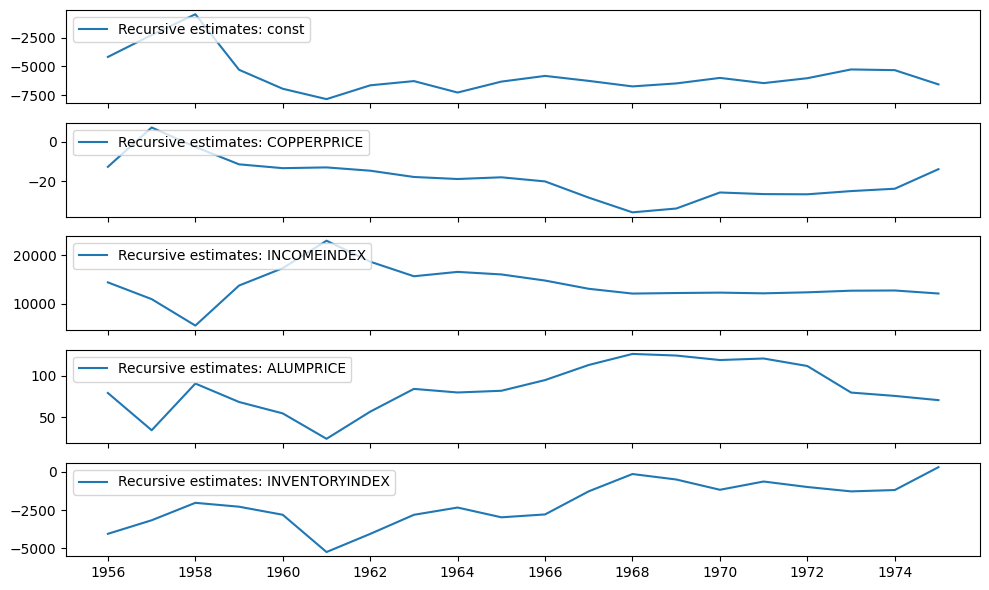

再帰係数は recursive_coefficients 属性で使用できます。または、 plot_recursive_coefficient メソッドを使用してプロットを生成することもできます。

[4]:

print(res.recursive_coefficients.filtered[0])

res.plot_recursive_coefficient(range(mod.k_exog), alpha=None, figsize=(10, 6))

[ 2.88890087 4.94795049 1558.41803044 1958.43326658

-51474.9578655 -4168.94974192 -2252.61351128 -446.55908507

-5288.39794736 -6942.31935786 -7846.0890355 -6643.15121393

-6274.11015558 -7272.01696292 -6319.02648554 -5822.23929148

-6256.30902754 -6737.4044603 -6477.42841448 -5995.90746904

-6450.80677813 -6022.92166487 -5258.35152753 -5320.89136363

-6562.37193573]

[4]:

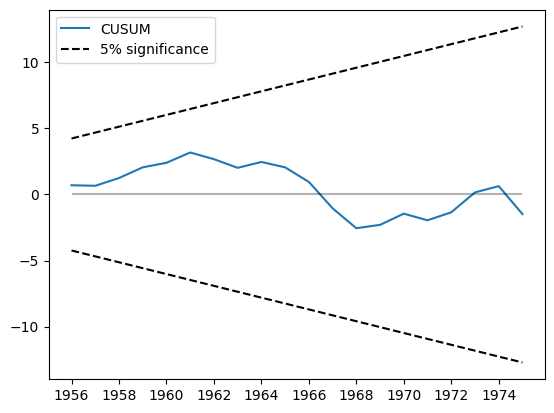

CUSUM統計量はcusum属性で利用できますが、通常はplot_cusumメソッドを使用してパラメータの安定性を視覚的に確認する方が便利です。下のプロットでは、CUSUM統計量が5%の有意水準帯を超えていないため、5%の水準で安定したパラメータの帰無仮説を棄却できません。

[5]:

print(res.cusum)

fig = res.plot_cusum()

[ 0.69971508 0.65841244 1.24629674 2.05476032 2.39888918 3.1786198

2.67244672 2.01783215 2.46131747 2.05268638 0.95054336 -1.04505546

-2.55465286 -2.29908152 -1.45289492 -1.95353993 -1.3504662 0.15789829

0.6328653 -1.48184586]

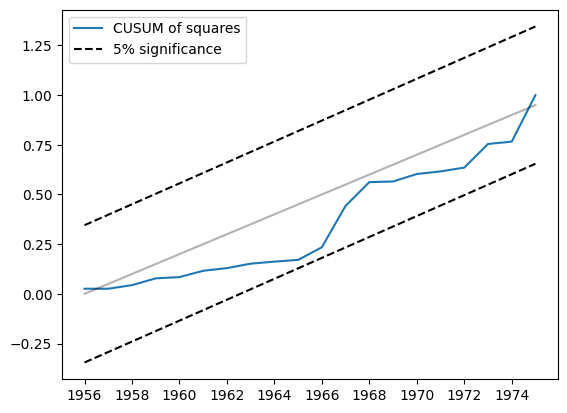

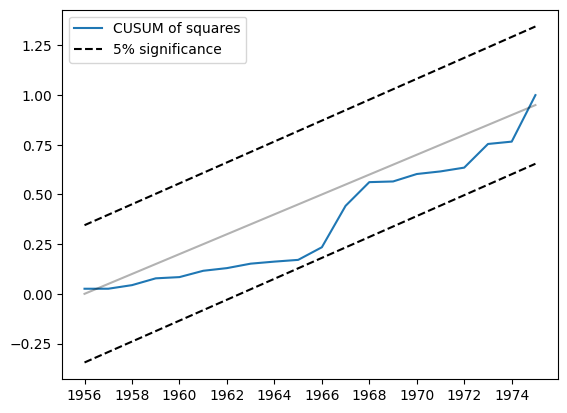

もう一つ関連する統計量は、二乗和のCUSUMです。これはcusum_squares属性で確認できますが、視覚的に確認する方が便利であり、そのためにplot_cusum_squaresメソッドが用意されています。以下のプロットでは、二乗和のCUSUM統計量は5%の有意水準バンドの外に出ていないため、5%の有意水準で安定したパラメータの帰無仮説を棄却できません。

[6]:

res.plot_cusum_squares()

[6]:

例2: 貨幣数量説¶

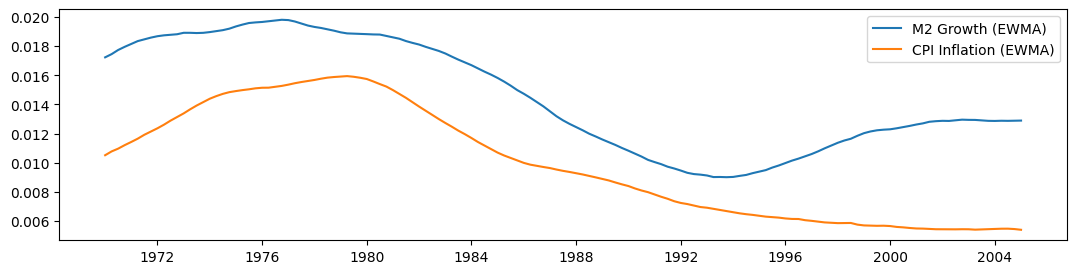

貨幣数量説は、「貨幣供給量の変化率の変化が与えられた場合、それは…物価上昇率の変化と等しい変化を引き起こす」と示唆しています(Lucas, 1980)。Lucasに従い、私たちは貨幣成長の両面指数加重移動平均とCPIインフレ率との関係を調べます。Lucasはこれらの変数間の関係が安定していることを発見しましたが、最近ではこの関係が不安定であるようです。例えば、SargentとSurico(2010)を参照してください。

[7]:

start = "1959-12-01"

end = "2015-01-01"

m2 = DataReader("M2SL", "fred", start=start, end=end)

cpi = DataReader("CPIAUCSL", "fred", start=start, end=end)

[8]:

def ewma(series, beta, n_window):

nobs = len(series)

scalar = (1 - beta) / (1 + beta)

ma = []

k = np.arange(n_window, 0, -1)

weights = np.r_[beta ** k, 1, beta ** k[::-1]]

for t in range(n_window, nobs - n_window):

window = series.iloc[t - n_window : t + n_window + 1].values

ma.append(scalar * np.sum(weights * window))

return pd.Series(ma, name=series.name, index=series.iloc[n_window:-n_window].index)

m2_ewma = ewma(np.log(m2["M2SL"].resample("QS").mean()).diff().iloc[1:], 0.95, 10 * 4)

cpi_ewma = ewma(

np.log(cpi["CPIAUCSL"].resample("QS").mean()).diff().iloc[1:], 0.95, 10 * 4

)

ルーカスの\(\beta = 0.95\)フィルター(両側に10年のウィンドウを使用)を使って移動平均を構築した後、以下に各シリーズをプロットします。サンプルの一部ではそれらが一緒に動いているように見えますが、1990年以降はそれらが分岐しているように見えます。

[9]:

fig, ax = plt.subplots(figsize=(13, 3))

ax.plot(m2_ewma, label="M2 Growth (EWMA)")

ax.plot(cpi_ewma, label="CPI Inflation (EWMA)")

ax.legend()

[9]:

<matplotlib.legend.Legend at 0x246e0a5ff10>

[10]:

endog = cpi_ewma

exog = sm.add_constant(m2_ewma)

exog.columns = ["const", "M2"]

mod = sm.RecursiveLS(endog, exog)

res = mod.fit()

print(res.summary())

Statespace Model Results

==============================================================================

Dep. Variable: CPIAUCSL No. Observations: 141

Model: RecursiveLS Log Likelihood 692.328

Date: Thu, 28 Nov 2024 R-squared: 0.812

Time: 23:11:20 AIC -1380.656

Sample: 01-01-1970 BIC -1374.758

- 01-01-2005 HQIC -1378.259

Covariance Type: nonrobust Scale 0.000

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

const -0.0034 0.001 -6.002 0.000 -0.004 -0.002

M2 0.9133 0.037 24.482 0.000 0.840 0.986

===================================================================================

Ljung-Box (L1) (Q): 138.24 Jarque-Bera (JB): 18.28

Prob(Q): 0.00 Prob(JB): 0.00

Heteroskedasticity (H): 5.36 Skew: -0.81

Prob(H) (two-sided): 0.00 Kurtosis: 2.28

===================================================================================

Warnings:

[1] Parameters and covariance matrix estimates are RLS estimates conditional on the entire sample.

[11]:

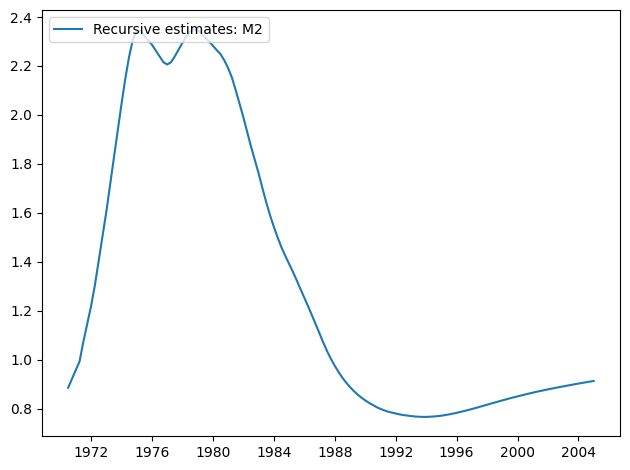

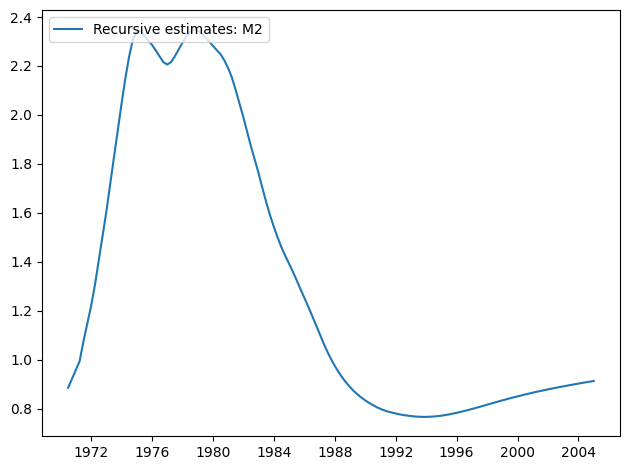

res.plot_recursive_coefficient(1, alpha=None)

[11]:

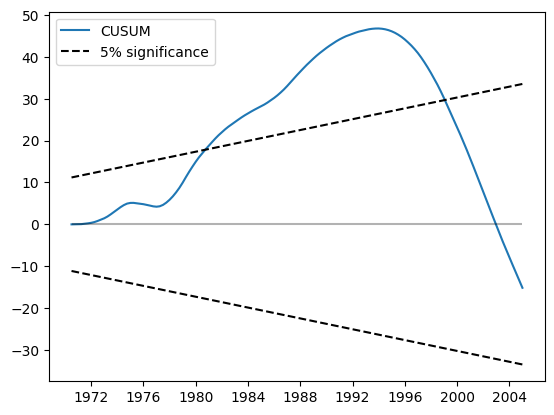

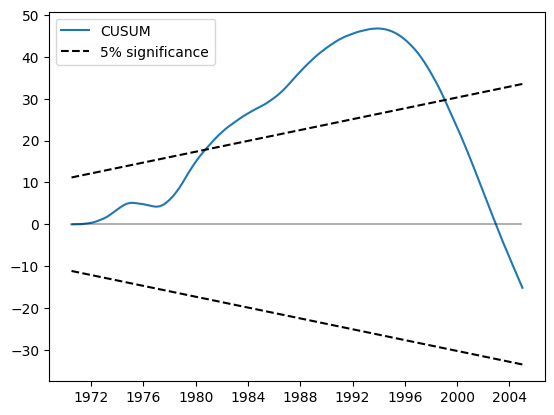

CUSUM プロットは 5% レベルで大幅な偏差を示しており、パラメータ安定性の帰無仮説が棄却されたことを示しています。

[12]:

res.plot_cusum()

[12]:

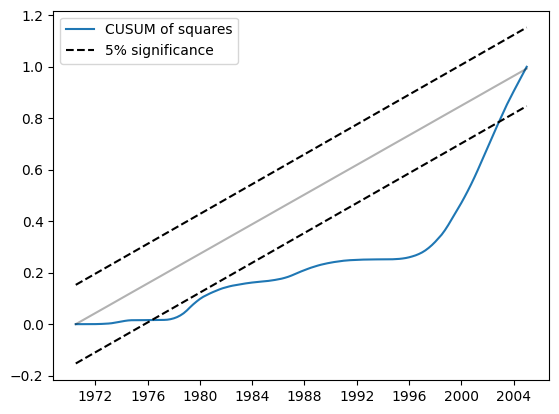

同様に、二乗の CUSUM は 5% レベルで大幅な偏差を示しており、これもパラメータ安定性の帰無仮説が棄却されることを示唆しています。

[13]:

res.plot_cusum_squares()

[13]:

例3: 線形制約と式¶

線形制約¶

モデルを構築する際に、constraintsパラメータを使用することで、線形制約を実装することは難しくありません。

[14]:

endog = dta["WORLDCONSUMPTION"]

exog = sm.add_constant(

dta[["COPPERPRICE", "INCOMEINDEX", "ALUMPRICE", "INVENTORYINDEX"]]

)

mod = sm.RecursiveLS(endog, exog, constraints="COPPERPRICE = ALUMPRICE")

res = mod.fit()

print(res.summary())

Statespace Model Results

==============================================================================

Dep. Variable: WORLDCONSUMPTION No. Observations: 25

Model: RecursiveLS Log Likelihood -134.231

Date: Thu, 28 Nov 2024 R-squared: 0.989

Time: 23:11:23 AIC 276.462

Sample: 01-01-1951 BIC 281.338

- 01-01-1975 HQIC 277.814

Covariance Type: nonrobust Scale 137155.014

==================================================================================

coef std err z P>|z| [0.025 0.975]

----------------------------------------------------------------------------------

const -4839.4836 2412.410 -2.006 0.045 -9567.721 -111.246

COPPERPRICE 5.9797 12.704 0.471 0.638 -18.921 30.880

INCOMEINDEX 1.115e+04 666.308 16.738 0.000 9847.000 1.25e+04

ALUMPRICE 5.9797 12.704 0.471 0.638 -18.921 30.880

INVENTORYINDEX 241.3452 2298.951 0.105 0.916 -4264.515 4747.206

===================================================================================

Ljung-Box (L1) (Q): 6.27 Jarque-Bera (JB): 1.78

Prob(Q): 0.01 Prob(JB): 0.41

Heteroskedasticity (H): 1.75 Skew: -0.63

Prob(H) (two-sided): 0.48 Kurtosis: 2.32

===================================================================================

Warnings:

[1] Parameters and covariance matrix estimates are RLS estimates conditional on the entire sample.

式¶

同じモデルをクラスメソッドfrom_formulaを使ってフィットさせることができます。

[15]:

mod = sm.RecursiveLS.from_formula(

"WORLDCONSUMPTION ~ COPPERPRICE + INCOMEINDEX + ALUMPRICE + INVENTORYINDEX",

dta,

constraints="COPPERPRICE = ALUMPRICE",

)

res = mod.fit()

print(res.summary())

Statespace Model Results

==============================================================================

Dep. Variable: WORLDCONSUMPTION No. Observations: 25

Model: RecursiveLS Log Likelihood -134.231

Date: Thu, 28 Nov 2024 R-squared: 0.989

Time: 23:11:23 AIC 276.462

Sample: 01-01-1951 BIC 281.338

- 01-01-1975 HQIC 277.814

Covariance Type: nonrobust Scale 137155.014

==================================================================================

coef std err z P>|z| [0.025 0.975]

----------------------------------------------------------------------------------

Intercept -4839.4836 2412.410 -2.006 0.045 -9567.721 -111.246

COPPERPRICE 5.9797 12.704 0.471 0.638 -18.921 30.880

INCOMEINDEX 1.115e+04 666.308 16.738 0.000 9847.000 1.25e+04

ALUMPRICE 5.9797 12.704 0.471 0.638 -18.921 30.880

INVENTORYINDEX 241.3452 2298.951 0.105 0.916 -4264.515 4747.206

===================================================================================

Ljung-Box (L1) (Q): 6.27 Jarque-Bera (JB): 1.78

Prob(Q): 0.01 Prob(JB): 0.41

Heteroskedasticity (H): 1.75 Skew: -0.63

Prob(H) (two-sided): 0.48 Kurtosis: 2.32

===================================================================================

Warnings:

[1] Parameters and covariance matrix estimates are RLS estimates conditional on the entire sample.

C:\Users\user\projects\statsmodels-main\statsmodels\tsa\base\tsa_model.py:465: ValueWarning: No frequency information was provided, so inferred frequency YS-JAN will be used.

self._init_dates(dates, freq)