失業率のトレンドとサイクル¶

ここでは、経済データにおけるトレンドとサイクルを分離するための3つの方法を考えます。時系列 \(y_t\) が与えられていると仮定し、基本的なアイデアはこれを2つの成分に分解することです:

ここで、\(\mu_t\) はトレンドまたはレベルを表し、\(\eta_t\) はサイクル成分を表します。この場合、確率的トレンドを考慮し、\(\mu_t\) はランダム変数であり、時間の決定論的関数ではないとします。3つの方法のうち2つは「未観測成分」モデルに分類され、3番目は一般的なホドリック・プレスコット(HP)フィルターです。Harvey and Jaeger(1993)などと一致するように、これらのモデルはすべて似たような分解を生成することが分かります。

このノートブックでは、これらのモデルを適用して米国の失業率におけるトレンドとサイクルを分離する方法を示します。

[1]:

%matplotlib inline

[2]:

import numpy as np

import pandas as pd

import statsmodels.api as sm

import matplotlib.pyplot as plt

[3]:

from pandas_datareader.data import DataReader

endog = DataReader('UNRATE', 'fred', start='1954-01-01')

endog.index.freq = endog.index.inferred_freq

ホドリック・プレスコット(HP)フィルター¶

最初の方法はホドリック・プレスコットフィルターで、これはデータ系列に非常に直感的に適用できます。ここでは、失業率が月次で観測されるため、パラメータ\(\lambda=129600\)を指定します。

[4]:

hp_cycle, hp_trend = sm.tsa.filters.hpfilter(endog, lamb=129600)

観測されない成分とARIMAモデル(UC-ARIMA)¶

次の方法は、観測されない成分モデルで、ここではトレンドがランダムウォークとしてモデル化され、サイクルはARIMAモデルでモデル化されます。特に、ここではAR(4)モデルを使用します。時系列のプロセスは次のように表すことができます:

ここで、\(\phi(L)\)はAR(4)のラグ多項式であり、\(\epsilon_t\)と\(\nu_t\)はホワイトノイズです。

[5]:

mod_ucarima = sm.tsa.UnobservedComponents(endog, 'rwalk', autoregressive=4)

# Here the powell method is used, since it achieves a

# higher loglikelihood than the default L-BFGS method

res_ucarima = mod_ucarima.fit(method='powell', disp=False)

print(res_ucarima.summary())

Unobserved Components Results

==============================================================================

Dep. Variable: UNRATE No. Observations: 847

Model: random walk Log Likelihood -463.600

+ AR(4) AIC 939.201

Date: Wed, 28 Aug 2024 BIC 967.644

Time: 14:38:13 HQIC 950.099

Sample: 01-01-1954

- 07-01-2024

Covariance Type: opg

================================================================================

coef std err z P>|z| [0.025 0.975]

--------------------------------------------------------------------------------

sigma2.level 6.057e-08 0.011 5.47e-06 1.000 -0.022 0.022

sigma2.ar 0.1747 0.015 11.774 0.000 0.146 0.204

ar.L1 1.0258 0.019 54.132 0.000 0.989 1.063

ar.L2 -0.1060 0.016 -6.612 0.000 -0.137 -0.075

ar.L3 0.0755 0.023 3.264 0.001 0.030 0.121

ar.L4 -0.0268 0.019 -1.422 0.155 -0.064 0.010

===================================================================================

Ljung-Box (L1) (Q): 0.00 Jarque-Bera (JB): 6636081.73

Prob(Q): 0.97 Prob(JB): 0.00

Heteroskedasticity (H): 9.13 Skew: 17.45

Prob(H) (two-sided): 0.00 Kurtosis: 435.48

===================================================================================

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).

確率的サイクルを持つ未観測成分モデル (UC)¶

最終的な方法も未観測成分モデルですが、ここではサイクルが明示的にモデル化されています。

[6]:

mod_uc = sm.tsa.UnobservedComponents(

endog, 'rwalk',

cycle=True, stochastic_cycle=True, damped_cycle=True,

)

# Here the powell method gets close to the optimum

res_uc = mod_uc.fit(method='powell', disp=False)

# but to get to the highest loglikelihood we do a

# second round using the L-BFGS method.

res_uc = mod_uc.fit(res_uc.params, disp=False)

print(res_uc.summary())

Unobserved Components Results

=====================================================================================

Dep. Variable: UNRATE No. Observations: 847

Model: random walk Log Likelihood -472.370

+ damped stochastic cycle AIC 952.740

Date: Wed, 28 Aug 2024 BIC 971.693

Time: 14:38:13 HQIC 960.002

Sample: 01-01-1954

- 07-01-2024

Covariance Type: opg

===================================================================================

coef std err z P>|z| [0.025 0.975]

-----------------------------------------------------------------------------------

sigma2.level 0.0177 0.032 0.547 0.585 -0.046 0.081

sigma2.cycle 0.1546 0.032 4.866 0.000 0.092 0.217

frequency.cycle 0.0436 0.029 1.508 0.131 -0.013 0.100

damping.cycle 0.9564 0.019 51.381 0.000 0.920 0.993

===================================================================================

Ljung-Box (L1) (Q): 1.53 Jarque-Bera (JB): 6534930.78

Prob(Q): 0.22 Prob(JB): 0.00

Heteroskedasticity (H): 9.48 Skew: 17.30

Prob(H) (two-sided): 0.00 Kurtosis: 432.69

===================================================================================

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).

グラフィカル比較¶

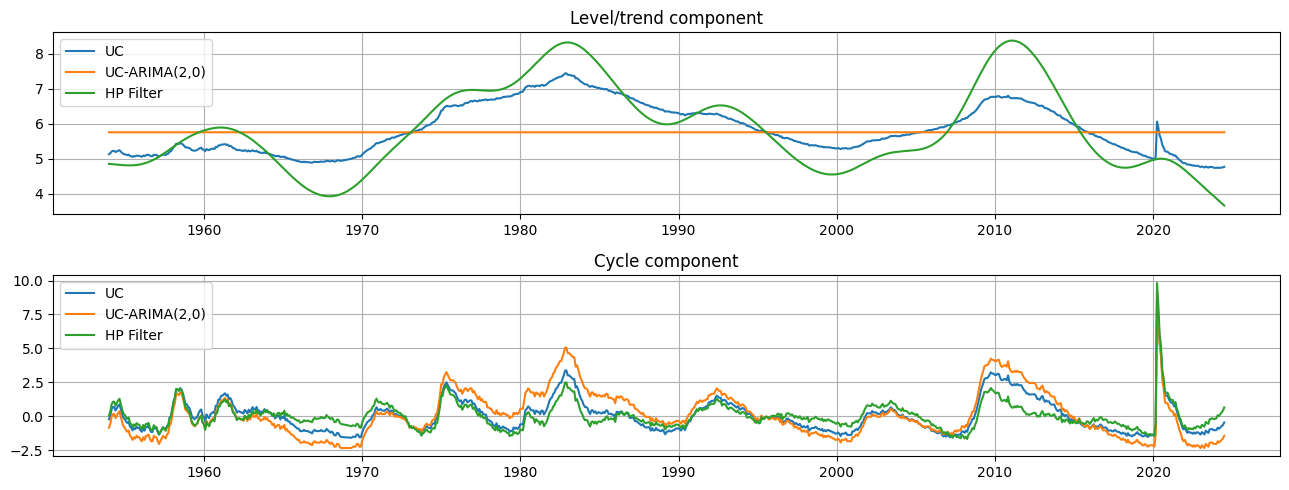

これらの各モデルの出力は、トレンド成分 \(\mu_t\) と循環成分 \(\eta_t\) の推定値です。定性的には、トレンドとサイクルの推定値は非常に似ているものの、HPフィルターによるトレンド成分は、観測されない成分モデルによるものよりもやや変動が大きいです。これは、失業率の動きの比較的多くが一時的な循環的動きではなく、基礎的なトレンドの変化に起因していることを意味します。

[7]:

fig, axes = plt.subplots(2, figsize=(13,5));

axes[0].set(title='Level/trend component')

axes[0].plot(endog.index, res_uc.level.smoothed, label='UC')

axes[0].plot(endog.index, res_ucarima.level.smoothed, label='UC-ARIMA(2,0)')

axes[0].plot(hp_trend, label='HP Filter')

axes[0].legend(loc='upper left')

axes[0].grid()

axes[1].set(title='Cycle component')

axes[1].plot(endog.index, res_uc.cycle.smoothed, label='UC')

axes[1].plot(endog.index, res_ucarima.autoregressive.smoothed, label='UC-ARIMA(2,0)')

axes[1].plot(hp_cycle, label='HP Filter')

axes[1].legend(loc='upper left')

axes[1].grid()

fig.tight_layout();